Managing your company’s fixed asset tool is a complicated process, one that will require some extra assistance.

Much of the work you do in QuickBooks is short-term. You send an invoice and it gets paid. Your purchase order is fulfilled, and the products move into your inventory. You run payrolls and submit their related taxes and other payments.

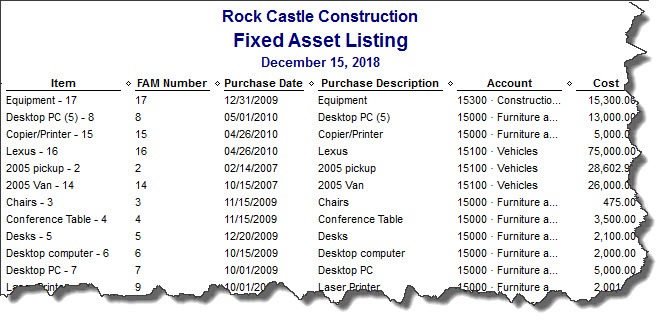

Managing the life cycle of your fixed assets is an exception. Simply, fixed assets are physical entities that you purchase to help your business generate revenue, like property, a vehicle, or a commercial oven. By definition, they must be in use for over 12 months.

You’ll need our help in depreciating the book value of your fixed assets, but careful recording of them will make your QuickBooks reports, your taxes, and your company’s worth more accurate.

QuickBooks can help you track these, but both the value of your company and your tax obligations – and the sale price, should you eventually sell them — are affected by how the book value of your fixed assets is depreciated. It’s important that you work closely with us over the life of each one. What you can do on your own, though, is to maintain absolutely accurate records in this area.

Two Paths

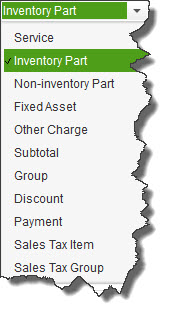

The best time to start recording information about a fixed asset is while you’re creating a transaction related to its purchase. You can build an item record for it as you’re filling out the Item section of Enter Bills, Write Checks, Enter Credit Card Charges or Purchase Order.

Let’s say you’re writing a check for a new company truck. You’d go to Banking | Write Checks and fill in the blanks. Click the Items tab below the MEMO field, then click the down arrow in the ITEM field. Scroll up to the top of the list if necessary and select <Add New>. You’ll see this menu:

Keep track of your

company’s fixed assets

by creating item records

for them. You can do

this as you’re entering

transactions for their

purchase.

Click on Fixed Asset to open the New Item window.

Transactions Not Required

There may be times when you’ll want to create an item record for a fixed asset when you’re not processing a transaction. Such situations include:

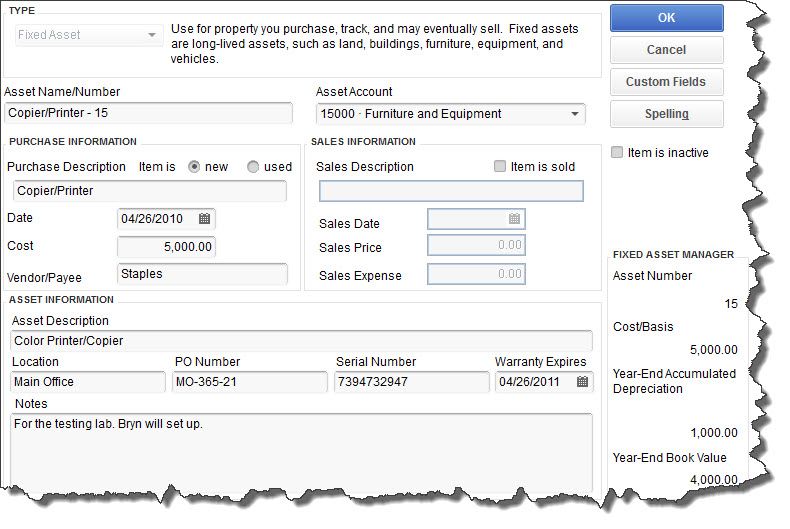

To do this, click on the Lists menu and select Fixed Asset Item List. If you’re adding a new one, right-click anywhere in the list part of the screen and select New (or click the down arrow next to the Item button in the lower left of the screen and click New). The same New Item window that you opened from the check-writing screen appears.

You’ve already chosen Fixed Asset as the TYPE, so your cursor should be in the Asset Name/Number field. Enter an easy-to-recognize name so that you’ll be able to quickly identify it in reports. Select the correct Asset Account (ask us if you’re not sure) and type a description in the Purchase Description field, clicking the correct button for new or used.

Enter the Date purchased, the Cost and the Vendor/Payee. Don’t worry about the SALES INFORMATION fields until – and if – you eventually sell the asset.

You should be able to complete the New Item window in QuickBooks for your fixed assets on your own, but consult with us on any questions.

Under ASSET INFORMATION, enter the Asset Description (you can write a lengthier description here), its Location, PO Number if applicable, Serial Number, and warranty expiration date. Add Notes if you’d like, and you’re done – unless you want to incorporate Custom Fields. If so, click the Custom Fields button in the upper right, then Define Fields.

(We can provide the depreciation and book value numbers under FIXED ASSET MANAGER.)

Your fixed asset records are critical elements of QuickBooks. You may be storing similar information elsewhere in your office records, but QuickBooks needs it, too, so you’ll have a comprehensive accounting of your company’s value.